The proposal also aims to address challenges in the area of VAT raised by the development of the platform economy.

Member States lost €93 billion in VAT revenues in 2020 according to the 2022 VAT Gap report. Conservative estimates suggest that one quarter of the missing revenues can be attributed directly to VAT fraud linked to intra-EU trade. In addition, VAT arrangements in the EU can still be burdensome for businesses, especially for SMEs, scale-ups and other companies who operate cross-border.

Key actions proposed will help Member States collect up to €18 billion more in VAT revenues annually (€11 billion as a result of anti-fraud measures) while helping businesses, including SMEs, to grow:

A move to real-time digital reporting based on e-invoicing for businesses that operate cross-border in the EU

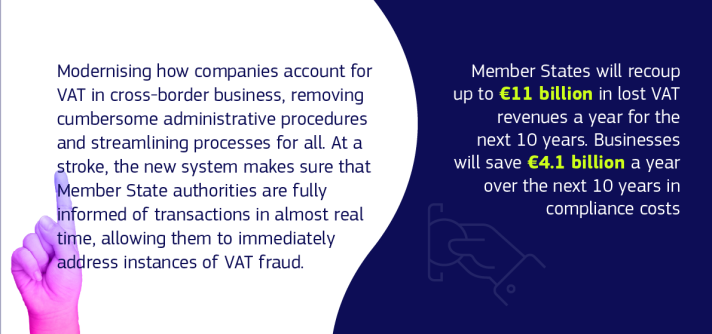

The new system introduces real-time digital reporting for VAT purposes based on e-invoicing that will give Member States valuable information they need to step up the fight against VAT fraud, especially carousel fraud. The move to e-invoicing will help reduce VAT fraud by up to €11 billion a year and bring down administrative and compliance costs for EU traders by over €4.1 billion per year over the next ten years. It also makes sure that existing national systems converge across the EU and paves the way for Member States that wish to set up national digital reporting systems for domestic trade in the coming years.

Updated VAT rules for passenger transport and short-term accommodation platforms

Under the new rules, platform economy operators in those sectors will become responsible for collecting and remitting VAT to tax authorities when their users do not, for example because they are a small business or individual provider. Together with other clarifications, this will ensure a uniform approach across all Member States and contribute to a more level playing field between online and traditional short-term accommodation and transport services. It will also whilst simplifying life for SMEs who would need to understand and comply with the VAT rules, often in other Member States.

The introduction of a single VAT registration across the EU

Building on the already existing ‘VAT One Stop Shop’ model for online shopping companies, the proposals would allow businesses selling to consumers in another Member State to register only once for VAT purposes for the entire EU, and to fulfil their VAT obligations via a single online portal in one single language. Further measures to improve the collection of VAT include making the ‘Import One Stop Shop’ mandatory for certain platforms facilitating sales to consumers in the EU.