On the 17th April we organized a webinar on the new HOT proposal with offered a deep-dive into the proposal.

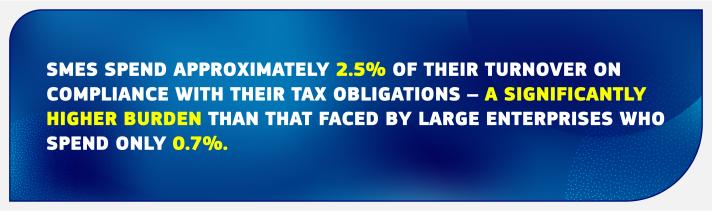

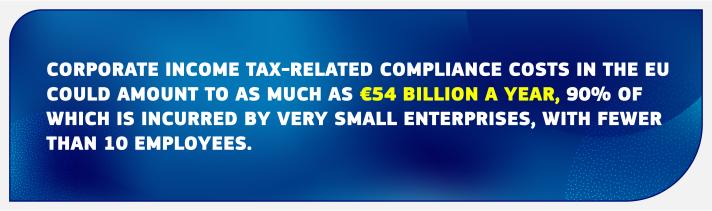

Compliance with business taxation rules can be complex. If SMEs wish to operate cross-border, they become taxable in more than one Member State as soon as their activity abroad creates a permanent establishment, which requires compliance with different tax systems and rules.

Compliance with those obligations comes with fixed costs, creating a barrier that can prevent SMEs from developing into other markets, investing back into their business or hiring new staff. This is especially the case for new companies and start-ups.

Under the new Head Office Taxation (HOT) proposal, cross-border SMEs would be able to choose to interact with only one tax administration in one EU Member State – that of the Head Office – instead of having to comply with multiple tax systems.

The Commission's proposal will increase tax certainty and reduce compliance costs, which will help to foster investment and cross-border expansion in the EU.

How will the new system work?

SMEs would calculate their taxable result for all their activities, in their main Member State (Head office Member State) and all their permanent establishments in the EU, using only the tax rules of the Member State where their Head Office is located.

They file one single tax return with the tax administration of that Member State.

The tax administration shares this return with the other Member States where the SME maintains a presence.

The Member State of the Head Office applies the tax rate of the other Member States to the profits accrued by the SMEs permanent establishment there and transfers any resulting tax revenues.

Eligibility, termination and anti-abuse

Once an SME chooses to apply the new rules, it will have to remain under this system for five fiscal years, unless the Head Office changes residence in the meantime, or their foreign business activity grows exponentially in comparison to the business activity in the Member State of origin. In that case, the rules cease to apply.

SMEs will be able to renew their choice every five years without limit as long as they continue to meet the eligibility requirements. These eligibility and termination provisions are designed to discourage potential tax planning practices, notably the deliberate transfer of the Head Office to a low-tax country.

At the same time, each Member State remains competent for audits of permanent establishments in their jurisdiction and can also request obligatory joint audits with other Member States.

Next steps

The Commission’s proposal must be agreed unanimously by all EU Member States in the Council before it can become law.

Promotional Materials

Below you can find the different assets that can be used for promoting the HOT proposal. New material will be uploaded on a regular basis.

Legislative Documents

More information

Questions and Answers on the Head Office Tax System for SMEs