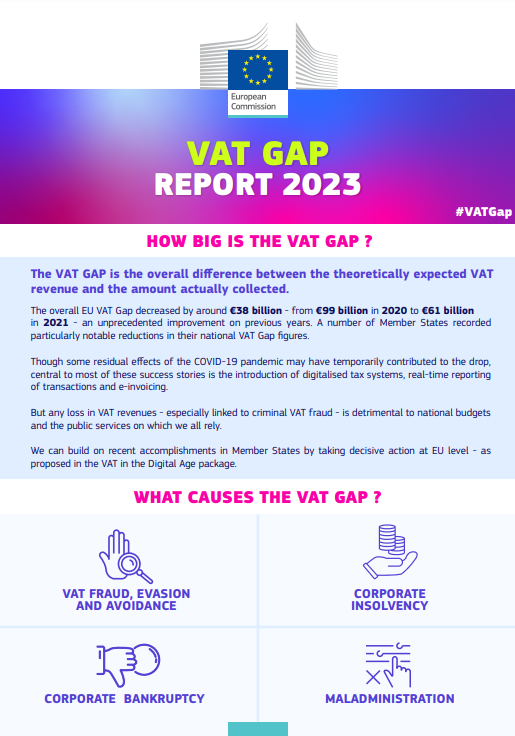

The ‘VAT Gap’ is the estimated difference between expected VAT revenue in the EU and the actual amount collected by EU countries. The European Commission monitors this difference because it has a direct impact on both EU and national budgets.

Report 2023

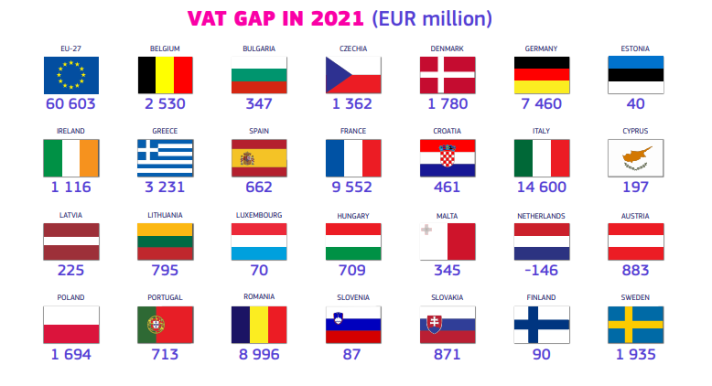

In 2021, most EU countries made progress in enforcing Value Added Tax (VAT) compliance, according to the 2023 VAT Gap Report released by the European Commission. The annual study shows that Member States lost around €61 billion in VAT in 2021, compared to €99 billion in 2020.

EU countries such as Italy (-10.7%) and Poland (-7.8%) recorded particularly notable reductions in their national VAT Gap figures, while the smallest gaps were observed in the Netherlands (-0.2%), Finland (0.4%), Spain (0.8%), and Estonia (1.4%).

The report shows that while some revenue losses are impossible to avoid, targeted policy responses seem to have made a difference, particularly those related to the digitalisation of tax systems, real-time reporting of transactions and e-invoicing.

Further downloads

| Country | Vat Gap in 2021 (EUR million) |

|---|---|

| Austria | 883 |

| Belgium | 2 530 |

| Bulgaria | 347 |

| Czechia | 1 362 |

| Croatia | 461 |

| Cyprus | 197 |

| Denmark | 1 780 |

| Estonia | 40 |

| Finland | 90 |

| France | 9 552 |

| Germany | 7 460 |

| Greece | 3 231 |

| Hungary | 709 |

| Ireland | 1 116 |

| Italy | 14 600 |

| Latvia | 225 |

| Lithuania | 795 |

| Luxembourg | 70 |

| Malta | 345 |

| Netherlands | -146 |

| Poland | 1 694 |

| Portugal | 713 |

| Romania | 8 996 |

| Slovakia | 871 |

| Slovenia | 87 |

| Spain | 662 |

| Sweden | 1 935 |

The VAT gap exists due to VAT fraud, evasion and avoidance, non-fraudulent bankruptcies, miscalculations and financial insolvencies, among other drivers.

Other circumstances that can influence the VAT Gap include economic developments, one-off government support measures and the quality of national statistics.

Relevance

Variations in VAT Gap estimations between EU countries reflect existing differences among Member States in terms of tax compliance, fraud, avoidance, bankruptcies, insolvencies and tax administration. It is important to monitor the VAT Gap since:

- VAT contributes to both national and EU budgets.

- The VAT Gap is a proxy of the performance of national tax administrations in their VAT collection.

- Lost VAT revenues have a negative impact on government spending on public goods and services such as schools, hospitals and transport.

- Studies on the scale of the VAT Gap help the Commission develop well-targeted measures to improve VAT compliance.

Reports 2009-2022

VAT compliance gap

VAT compliance gap due to Missing Trader Intra-Community (MTIC) fraud

A considerable portion of the intentional VAT non-compliance gap comes from MTIC fraud. MTIC fraud exploits the regulation for intra-community cross-border transactions, where VAT-registered suppliers can apply a zero rate on sales to other Member States' VAT-registered buyers. Fraudulent traders exploit this zero-rate intra-community supply by excluding subsequent fraudulent domestic supplies from their VAT returns.

To estimate the scale of the issue and how it evolves over time, a promising methodology leverages data from the VAT Information Exchange System (VIES) on intra-Community supplies, and similar reporting obligations on intra-Community acquisitions. The European Commission collaborates with Tax Administrations of Member States involved in the Tax Administrations in the EU Summit (TADEUS) project "Estimations of Tax Gap on PIT/SSC, CIT, MTIC fraud and VAT e-commerce" to gather data on intra-Community transactions. Information about the processing and protection of this individual-level data can be found in the privacy statement below.